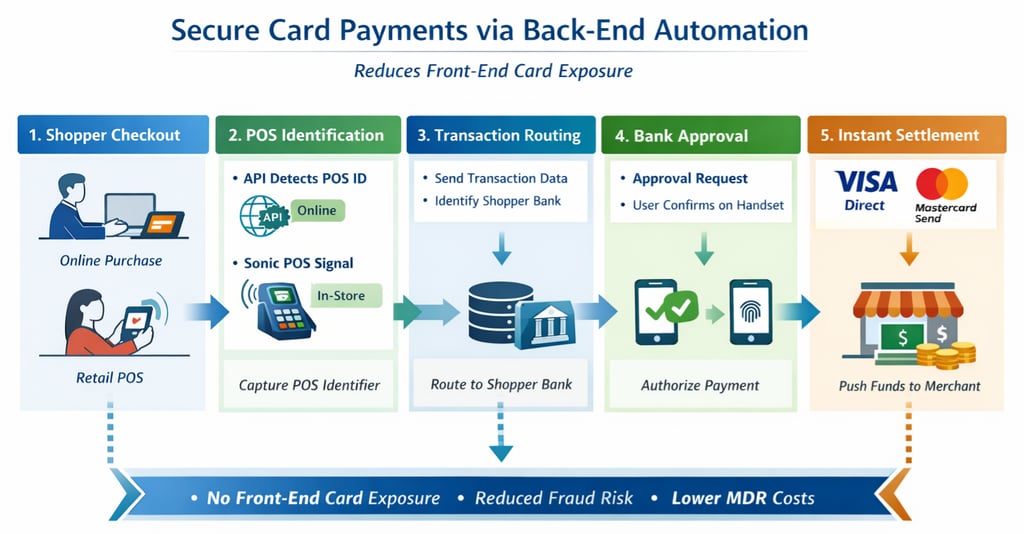

Automated Bank to Bank Payments

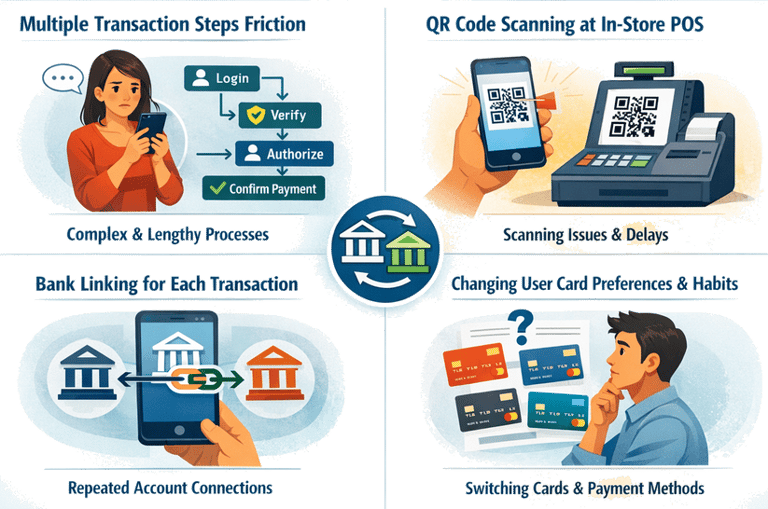

The Problem

Account‑to‑account (A2A) payments offer speed and cost advantages, but adoption faces several behavioral and technical hurdles. Multi‑step flows - such as scanning QR codes, linking bank accounts, and confirming each transaction - introduce friction that slows checkout and deters repeat use.

In‑store QR scanning often feels clunky compared to tap‑to‑pay, especially in high‑volume environments. Each transaction typically requires bank authentication, which adds latency and cognitive load. Moreover, users are accustomed to card‑based habits and loyalty programs, making it difficult to shift preferences.

These challenges limit A2A’s reach despite its efficiency. For A2A to scale, it must match the seamlessness of card payments while preserving its cost and fraud advantages - ideally through automated embedded flows, persistent bank links, and real‑time merchant recognition.

The Solution

A2A adoption can accelerate globally by removing front‑end friction and automating the checkout experience. Instead of requiring users to scan QR codes or repeatedly authenticate bank links, the system detects POS identifiers automatically - via APIs for online checkout or Sonic POS IDs captured by the shopper’s bank, mobile wallet, or merchant app during in‑store purchases.

Once detected, transaction data flows directly from the POS to the correct shopper bank using pre‑linked account information. The bank then issues a real‑time approval prompt on the shopper’s handset, which is confirmed by fingerprint or PIN. Funds are pushed instantly to the merchant through real‑time payment networks. This automated prompt model reduces friction, reshapes card habits, and makes A2A feel as seamless as tap‑to‑pay.

Transaction Flow